Podcast: Play in new window | Download

I think I can safely speak for all of us when I say we just want to put 2020 behind us. But there were a lot of lessons learned by credit unions in regards to credit vs debit payment trends during the pandemic, and that data will continue to prove useful throughout the rest of the pandemic and into the new normal.

To discuss how consumer debit and credit trends in 2020-21 have impacted the payments industry, how debit and credit transactions themselves have been impacted, and what changes should be expected across merchant sectors, PaymentsJournal sat down with Glynn Frechette, SVP, Advisors Plus Consulting at PSCU, Norm Patrick, Vice President, Advisors Plus Consulting at PSCU, and Ted Iacobuzio, VP and Managing Director of Research at Mercator Advisory Group.

Consumer debit and credit trends in 2020-21

Since the beginning of COVID-19, PSCU has been working on a weekly basis to analyze data on year-over-year changes and various payment dynamics. As a result of the pandemic, nobody was immune to the shifts in consumer behavior and payment patterns, which were heavily influenced by the adoption of new technologies. Although the pandemic was a largely negative occurrence, it did help to accelerate the implementation of more digital payment types and methods, which has been invaluable for the growth of the payments industry.

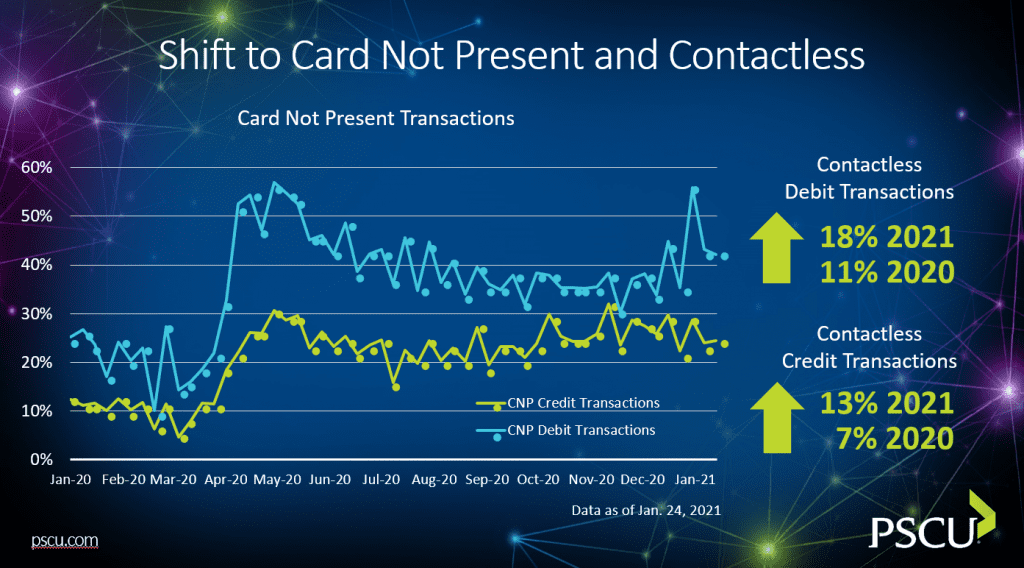

According to the chart below, there has been a substantial upward shift in contactless and card not present transactions. “The blue line shows our debit growth for Card Not Present transactions,” said Patrick. “And in our most current period, ending in January, we’re looking at about 42% year-over-year growth compared to credit card at 24.5% growth.”

While both numbers are impressive, there is an obvious gap between the debit and credit trends displayed. “I think you can attribute a lot of that to the fact that debit has really been the major growth in terms of payment method over the past year as we’ve gone through the pandemic,” explained Patrick. This could be due, in part, to a fear of fraudulent activity and a “my money versus their money” mindset.

In regards to contactless payments, the graph is not showing growth numbers. “These are actually share numbers,” added Patrick. “So it’s the percentage of contactless transactions that are conducted on contactless enabled debit cards or credit cards.” From 2020 to 2021, the debit side jumped up to 18% share, and the credit card up to 13%.

“I would even call these numbers a bit conservative, because not all merchants are able to take contactless; there have been more that have come live with it over time. And you know, that makes our numbers a bit conservative,” advised Patrick.

Mobile wallet transactions are also seeing a lot of growth, with 67.6% growth on debit, and 47.5% growth on credit. As more and more merchants add this technology to their stores, consumers will inevitably grow increasingly comfortable with leveraging it. “We’re beginning to see the fruits bear there as well.”

How have credit and debit card transactions been impacted?

Short answer: the impact has been significant.

PSCU has been working behind the scenes to address these credit and debit trends. “Spending remains very strong for both credit and debit, with growth in debit purchases in the goods, services and grocery sectors,” said Frechette. Unsurprisingly, this growth was aided by this second round of COVID-19 relief funding.

Debit card spending is up 23%, with debit transactions up 7% as of late January. That puts debit purchases in line with the four-week average growth of 25%, while transactions are slightly lower than the four-week average of 8%. “Credit card spend…in late January was up 3.8%, which is just below the four-week average of 4%, while transactions were down 3%,” continued Frechette.

Despite the unknowns of the long-term economic impact of COVID-19, consumers are choosing debit as their most preferred form of payment, which is in line with what PSCU has been reporting each week since late March. And according to PSCU’s 2020 Eye on Payments Study, this is the second full calendar year in a row that debit has remained the first preferred choice of payment method for consumers.

“Consumers are struggling with debt, and they find that using debit gives them more control over their finances. They’re more aware of the funds they have available to spend,” informed Frechette. They are paying more attention to the actual funds they have available to spend, and with the financial future of Americans feeling very uncertain, it makes sense that they’d choose to act responsibly.

While some financial institutions are focusing on debit because of the debit consumer trends that are at the forefront of this pandemic, “credit unions should not forget about promoting credit card programs,” warned Frechette. “It is a great time for credit unions to fill a need in the marketplace and grow their credit card portfolio.”

While credit unions should continue to encourage their customers to use their credit union issued cards at the point of sale, it is no longer enough. “Credit unions should be promoting incentives and special offers to encourage members to add or use their credit union issued cards over competing bank or Fintech issued cards,” suggested Frechette. PSCU can help credit unions enhance their incentive programs so that debit and credit transactions remain at the top of the wallet.

Changes across merchant sectors and consumer credit trends 2020

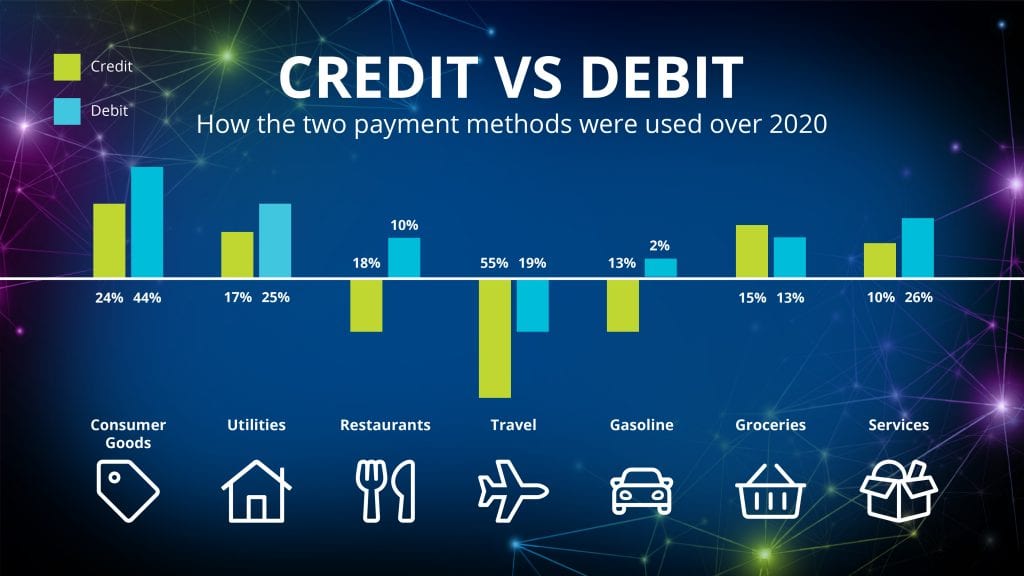

Across merchant sectors, there are winners, and there are losers. And the pandemic has certainly been calling the shots in terms of the successes and failures of merchants. “From the positive perspective, one of the bigger sectors of impact on the ‘good side’ has certainly been with consumer goods,” said Patrick.

Much of the spending that is occurring has been driven by improvements made to the home, such as general repairs and constructing home offices. According to the chart above, consumer goods were up 24% for the year so far for credit, and 44% for debit. Utilities spending is also up 25% year over year for debit and 17% for credit, which is most likely due to upgrades to the internet and heating the house more when working from home.

Services are also up, with about 26% for debit and 10% for credit. Groceries, however, have seen less growth since the initial panic of March and April has subsided. But there is still a 13% increase for debit and 15% increase for credit, which can most likely be attributed to people choosing to cook their meals at home rather than eat out.

This new preferred dining option, along with hourly and capacity restrictions and general fear of the virus, is one of the reasons restaurants are coming up short. Food establishments are actually up about 10% for debit, but down 18% for credit. Travel and gasoline are also being negatively impacted by the pandemic, with credit vs debit payment trends down for the 2020 spending year.

“That’s where things sit at today, knowing that at some point, we all hope we are going to head in a more positive direction relative to the pandemic,” offered Patrick. “With vaccine availability and [the] slowdown of the rampant infection rates, we would hope that at some point there is going to be release of pent-up demand.”

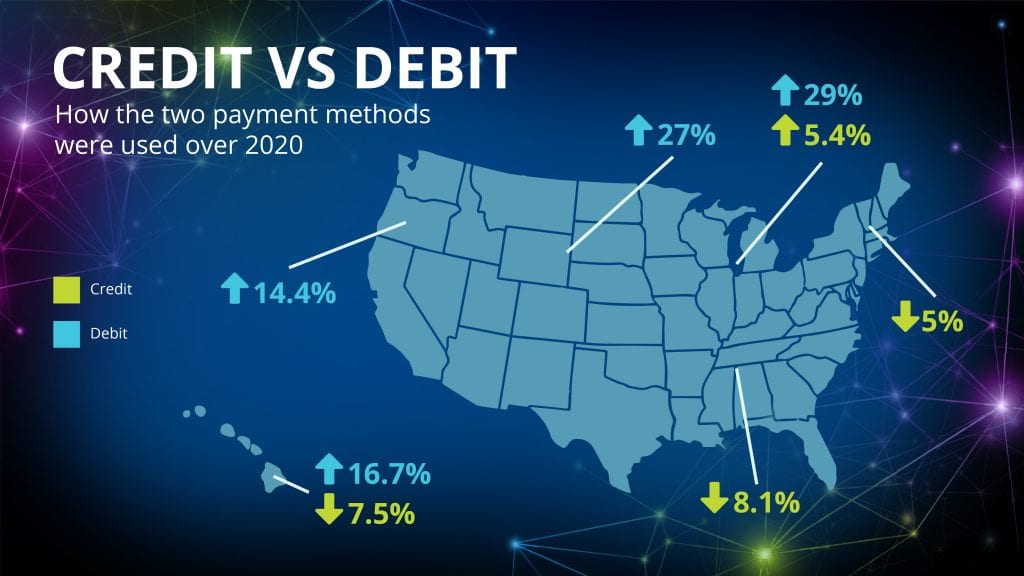

There were some additional interesting credit vs debit payment trends happening across the country. The overall U.S. spending coming out of January for credit cards was about 4%, with the Great Lakes Region up 5.4% and the Southeast up 8.1%. Those who did not perform quite as well were Hawaii, which was down 7.5%, and New England, down about 5%. Debit card trends showed spend up 23%, with the Great Lakes leading the pack (+29%), and the Plains Region coming up a close second (+27%). Hawaii and the West Coast both saw debit card transaction increases, at 16.7% and 14.4%, respectively.

“It’s been very interesting as we’ve gone through this to see these various patterns emerge [in credit and debit trends 2020] relative to the regions across the United States in addition to the merchant categories,” concluded Patrick.